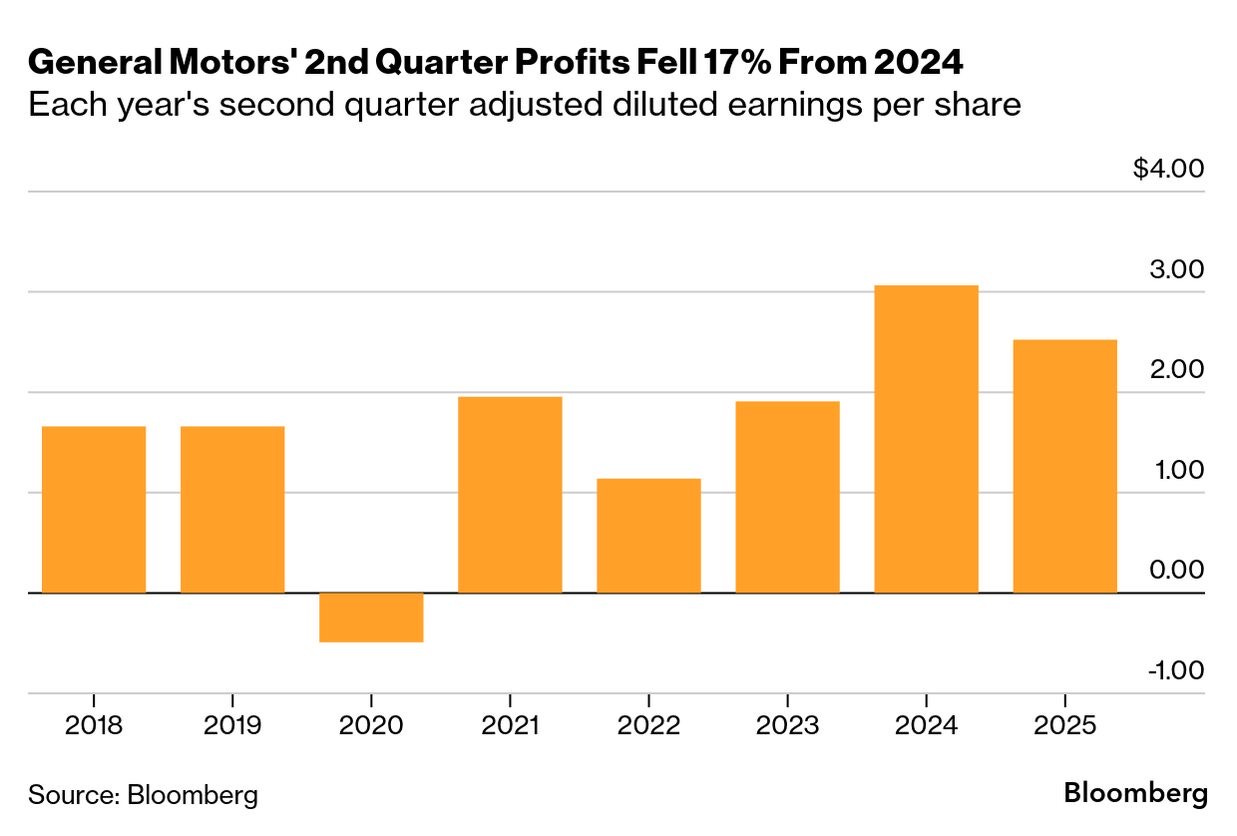

If you want to understand who’s really paying for Donald Trump’s tariffs, don’t look at Beijing, look in your driveway. Or more precisely, look at the earnings report from General Motors.

GM just disclosed that tariffs cost them over $1.1 billion in lost profits. Not because prices went up, but because they didn’t. The company chose to eat the cost instead of passing it on to consumers. That explains why car prices stayed flat in the June inflation data, even as prices for toys, appliances, and other imported goods jumped. In those cases, the costs are getting passed down, and the data proves it.

This isn’t theory anymore, it’s real-world impact. Tariffs are being paid by American businesses and, ultimately, American consumers. While the U.S. Treasury is enjoying a boost in customs revenue, those funds are coming out of domestic pockets. And foreign exporters aren’t lowering prices to compensate, as import price data makes clear.

As Deutsche Bank’s George Saravelos put it, “The top-down macro evidence seems clear: Americans are mostly paying for the tariffs.” And there’s more inflationary pressure in the pipeline.

Why this matters to real estate investors

Policy noise often gets ignored by our industry, until it becomes impossible to avoid. Tariffs increase the cost of goods, from appliances and finishes to construction materials. They also compress margins for domestic producers, which can reduce hiring and slow down regional economies. Both of those factors ripple through demand for housing, capex planning, and the feasibility of development projects.

We’re already seeing this play out in pro formas that were modeled with 2023 costs and 2025 realities. These macro disruptions force real estate developers like myself to rework assumptions mid-cycle, just to preserve solvency.

But tariffs are just one part of the storm.

The silent crisis brewing in private equity

Another red flag? The zombie apocalypse isn’t just for bad horror movies, it’s becoming a business headline.

In the world of private equity, the post-pandemic boom masked structural cracks in the middle of the capital stack. Now they’re starting to show. Midsize firms, those without the scale to diversify into insurance, infrastructure, or private credit, are stuck. They can’t exit deals at their target valuations, which means their LPs aren’t getting paid back, and fresh capital isn’t coming in.

The result is a growing class of “zombie funds” not failed firms, but frozen ones. No new deals, no growth, just a skeleton crew managing old investments, hoping for the market to turn. And with more than 18,000 private capital funds globally chasing $1 of dry powder for every $3 of demand, many of them are structurally unprepared to survive this moment.

For real estate sponsors, this matters. These same mid-tier PE shops are often the quiet co-GPs, mezz lenders, or LP equity partners behind a lot of real estate deals. If they go dark, liquidity dries up, not dramatically, but quietly, deal by deal, term sheet by term sheet.

Brightline and the illusion of momentum

If you’re looking for a metaphor for this whole moment, Brightline might be it.

Florida’s high-speed train from Miami to Orlando launched to great fanfare, a privately-backed vision for modern American rail. But earlier this month, Bloomberg reported Brightline was delaying an interest payment on $1.2 billion in bonds. The debt isn’t insignificant, and it’s spread across different layers and issuers, but the message is simple: just because a project launches doesn’t mean it’s financially sustainable.

We’ve all seen it in real estate too. Vision is exciting. Execution is harder. Debt is even harder when interest rates rise, timelines slip, and assumptions change.

The bottom line

These are not isolated data points. They’re signals, and if you’re in real estate or private capital, they should be loud ones. Tariffs are inflationary. Mid-market capital is freezing. Infrastructure ambition is colliding with balance sheet reality.

For those of us actively investing, the next 6 to 12 months are about discipline, optionality, and reading the room. Capital is still out there, but the cost of getting it, and keeping it, is rising. Navigating this moment means recalibrating not just your pro forma, but your partnerships and your pipeline.

The zombie firms won’t die tomorrow. The trains won’t stop running next week. But we’re already seeing who was built for volatility, and who was just surfing the cycle.

Daniel Kaufman is a real estate developer, investor, and managing director of Elevation Development. He leads projects across the country focused on workforce housing, build-to-rent communities, and infill urban revitalization.