We’re halfway through 2025, and the U.S. economy is flashing some familiar warning signs. Growth has slowed, consumer spending is softening, and the Federal Reserve just made it clear they’re not rushing to cut rates. For developers and investors, this isn’t just macro noise — it’s the backdrop we’re underwriting into.

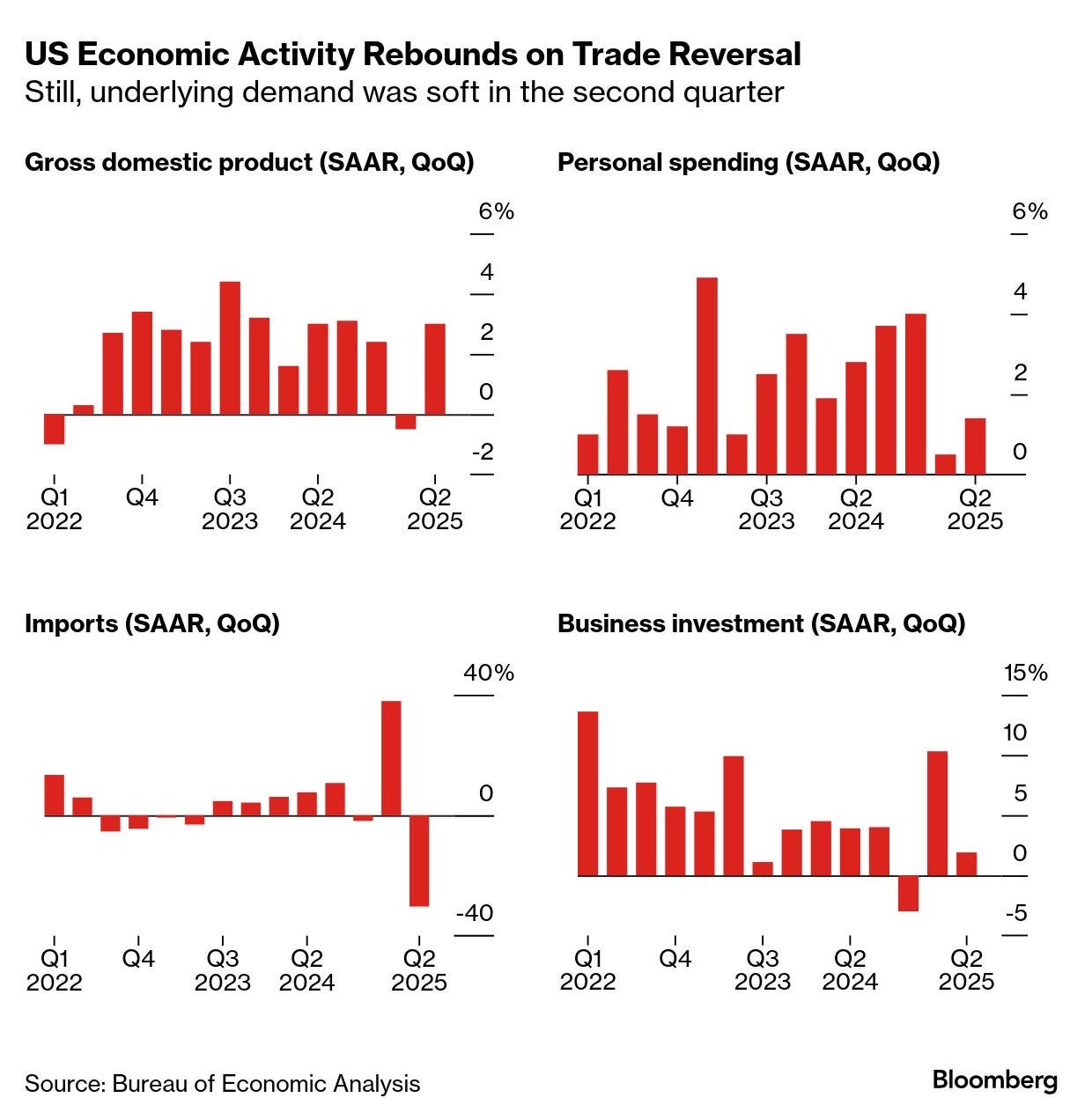

According to the latest GDP data, the economy expanded at an annualized rate of 3% in Q2. Not terrible. But if you average out the first half of the year, growth is sitting at 1.25% — a full point below where we were in 2024. That slowdown matters. It hits everything from tenant leasing velocity to exit cap assumptions.

The Fed Hits Pause, Again

Despite growing political pressure from Donald Trump — including not-so-veiled threats and plenty of social media theatrics — Fed Chair Jerome Powell isn’t budging. The FOMC held the federal funds rate steady at 4.25%–4.5% for the sixth consecutive meeting. Powell’s message? Rates are high enough, and uncertainty around tariffs and inflation is still too volatile to justify a cut.

That caution makes sense. Inflation may have moderated, but it’s nowhere near stable. The Fed’s independence is being openly challenged, and two Trump-aligned governors even voted for a rate cut — a sign of how politicized monetary policy could become if we enter another Trump term.

Why Developers Should Care

For those of us operating in ground-up development or value-add repositioning, this isn’t just theoretical. High rates continue to pressure deal economics. Construction loans remain expensive. Cap rates are sticky. And banks — still licking wounds from 2023’s regional banking mess — are slow to lend. If you’re not locking in predictable capital or stress-testing exit assumptions, you’re playing with fire.

Meanwhile, sellers who haven’t capitulated to today’s environment are still pricing to yesterday’s market. That’s created an unusual gap where deals aren’t penciling — but they’re also not being repriced quickly enough to create liquidity.

Then There’s the Trump Factor

Just when you think you’ve modeled the downside, Trump lobs another policy grenade. This week, he announced a 25% tariff on Indian exports starting August 1, while simultaneously threatening India over its energy deals with Russia. India, for its part, was actively negotiating a bilateral trade agreement with the U.S. after Modi’s February visit. That now appears to be unraveling.

At the same time, Trump backed off a sweeping copper tariff — and the market reacted instantly. Copper futures on Comex dropped over 19% in minutes, marking the largest intraday collapse ever recorded. Why does this matter for real estate? Because unpredictability in commodities markets can wreak havoc on construction pricing. If you’ve built a budget in the last 6 months, it probably needs another look.

How This All Ties Back to Real Estate

We’re in an environment where volatility is the only constant — politically, economically, and financially. The ground is shifting beneath our feet, whether we’re talking about the cost of drywall or the terms of sovereign trade. Developers, operators, and capital allocators need to read these signals in real time.

-

If you’re underwriting deals, stress test your rent growth assumptions.

-

If you’re raising capital, bake in longer timelines and tighter IRRs.

-

And if you’re trying to navigate construction, build in contingencies — both cost and time.

This isn’t a time for the faint of heart. But it is a time where those with discipline, dry powder, and patience can set themselves up for real upside when the dust settles.

Let the tourists chase rate cuts. We’ll be here, tightening our models, watching the tape, and preparing to strike when dislocation becomes opportunity.

Subscribe for more on market dislocations, development trends, and investment strategy at the intersection of policy, capital, and construction.