Last Friday, something snapped.

President Trump fired Erika McEntarfer, the head of the Bureau of Labor Statistics, after a weak jobs report showed unemployment rising. That decision, while shocking, was hardly surprising if you’ve been watching the drumbeat of executive overreach coming out of D.C. But for markets — and especially for investors who rely on data-driven pricing models — this could be the canary in the coal mine.

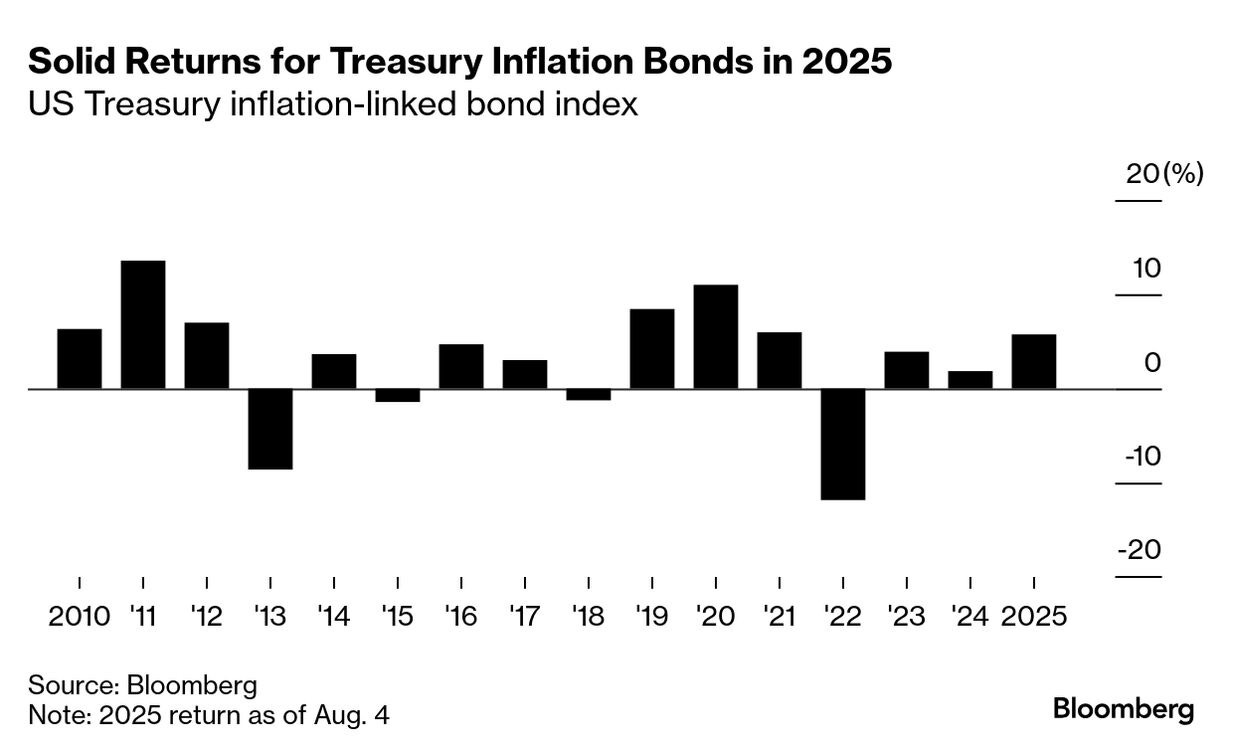

The $2 trillion Treasury inflation-protected securities (TIPS) market is particularly vulnerable. These securities are tied directly to CPI — which is calculated by, you guessed it, the BLS. If trust in that data erodes, the foundation of the entire asset class starts to wobble. And when institutional investors start questioning the validity of CPI, it’s not just a finance story anymore. It’s systemic.

Now, as someone who’s spent the last two decades developing real assets across dozens of U.S. markets, I know firsthand that confidence — in the Fed, in inflation prints, in interest rate policy — is often the most important invisible factor in any real estate deal. It’s what underpins our financing assumptions, our construction timelines, and our underwriting models. You can price in bad news. But you can’t price in chaos.

And that’s what this is starting to feel like.

A Fragile Data Ecosystem

Even before McEntarfer’s firing, there were quiet concerns about the durability of our “gold standard” economic data infrastructure. These independent agencies weren’t designed to survive being politicized. If they become mouthpieces — or worse, scapegoats — we’re in uncharted territory.

JPMorgan’s Michael Feroli put it plainly: “The integrity of this data is at least as important as the employment data.” And he’s right. Because with inflation once again creeping above the Fed’s 2% target, the stakes are enormous.

We’re entering a feedback loop: Trump’s tariffs are likely stoking inflation again, while he simultaneously demands rate cuts from the Fed. Then comes the pressure campaign to install a more compliant Fed chair. And if CPI data starts to look manipulated? The bond market won’t wait for confirmation. It will price in the uncertainty immediately.

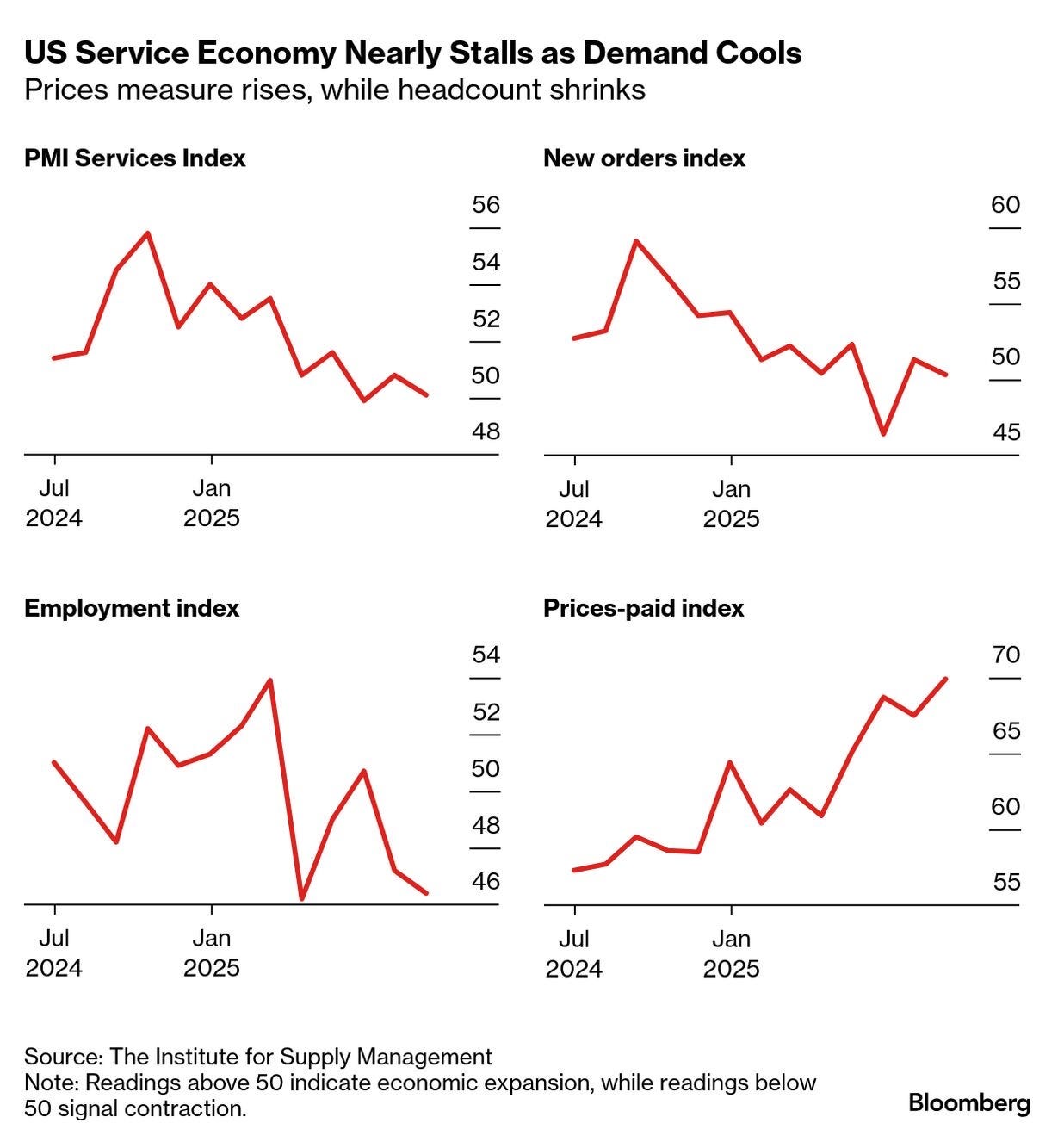

Beyond the BLS: Sluggish Services, Shaky Auctions

It’s not just government data sending up red flags. Private-sector indicators aren’t exactly giving us comfort either.

The Institute for Supply Management’s services index for July fell to 50.1 — barely above contraction territory. The employment sub-index dropped to 46.4, one of the worst post-pandemic readings we’ve seen. Demand is cooling, headcount is shrinking, and prices are rising. That’s not expansion. That’s stagflation creeping in through the side door.

So now we’re looking at a service sector that’s softening, inflation that’s stubborn, and a bond market that just absorbed a lackluster $58 billion three-year note auction. And all of this while the 10-year hovers at 4.20% and the Fed tiptoes around a politically hostile White House.

I’ve lived through enough cycles to know that the market rarely moves in a straight line. But we are in the middle of a structurally volatile moment. For developers and long-term investors like me, this is when we look less at short-term gains and more at how resilient our assets really are.

The Fed, the Dollar, and What Comes Next

Trump’s shortlist to replace Powell includes Kevin Warsh and Kevin Hassett — both of whom are more aligned with his views on aggressive rate cuts. Meanwhile, DoubleLine’s Bill Campbell is warning that the dollar is entering a multi-year decline, driven by ballooning deficits, dovish Fed pressure, and a crisis of investor confidence.

For context: the Republican tax cut and spending bill just added $3.4 trillion to an already massive deficit. Treasury Secretary Scott Bessent, for his part, is reportedly uninterested in replacing Powell — which might actually be the smartest move in this circus.

We’re talking about the dollar — the global reserve currency — at risk of further decline. We’re talking about inflation-linked bonds priced on possibly politicized data. And we’re talking about a real estate market (residential and commercial) that depends on stable rates, predictable yields, and trustworthy macro assumptions.

Final Thought

When trust in institutions erodes, capital moves accordingly. And it doesn’t always wait for confirmation. As a developer, that means I’m taking a harder look at interest rate sensitivity across my portfolio. As an investor, I’m watching how foreign capital is reacting to U.S. dollar risk. And as someone who’s made a career out of navigating market inflection points, I’ll say this: now is the time to be precise. In your assumptions. In your partnerships. In your exposure.

Because volatility isn’t just a Wall Street problem. It’s a Main Street problem — and it’s knocking.

Daniel Kaufman is a real estate developer, investor, and founder of Kaufman Development. He writes about markets, policy, and the intersection of capital and construction.