In a high-rate, low-liquidity world, self-storage is quietly stealing the spotlight.

Despite tighter capital markets, Q1 2025 saw $855 million in self-storage assets trade hands nationwide — a 37% jump year over year. Over 12 million square feet of facilities were sold, with the average price per SF hitting $117, up 31% from Q1 2024.

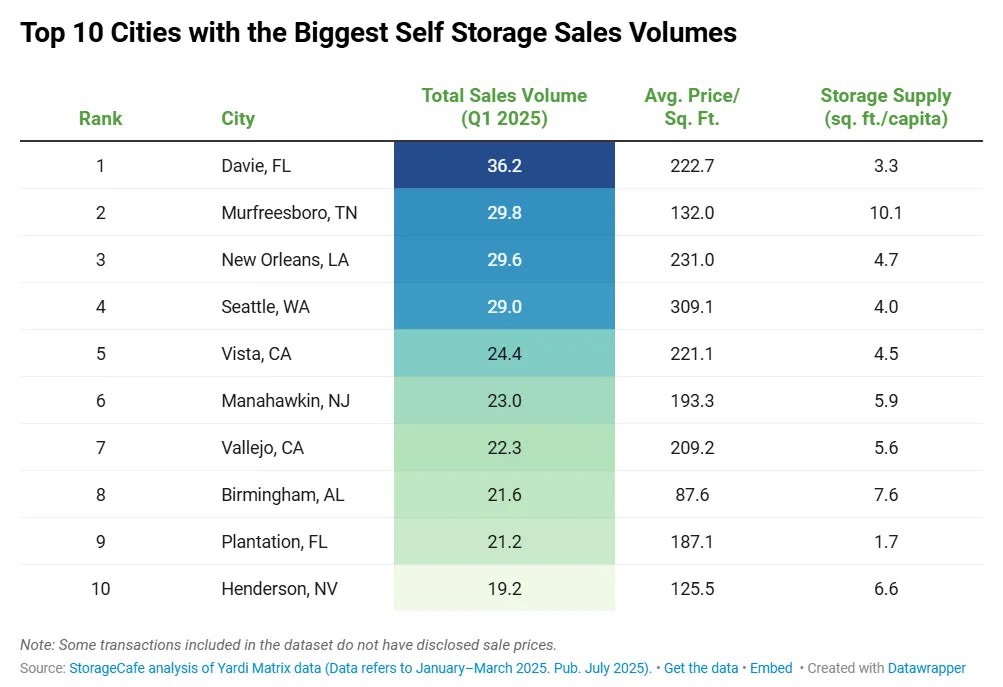

Biggest deal? Biggest price tag.

📍 Costa Mesa, CA led the nation with a jaw-dropping $387/SF — a clear signal of how supply shortages in high-density markets are driving values.

Other hotspots included:

-

Seattle, WA – $309/SF

-

Brookline, MA – $265/SF

Why the rush? It’s all about scarcity and demand.

Eight of the ten best-performing cities had below-average storage space per capita — giving investors the pricing power and long-term value they’re chasing.

Some standouts:

-

Davie, FL led with a $36M portfolio deal, even though the city offers just 3.3 SF of storage per resident.

-

Plantation, FL is even more undersupplied, at 1.7 SF per capita, despite significant population growth.

-

New Orleans and Seattle are seeing similar supply-demand tension, pushing rents higher and drawing major institutional capital.

Suburbs and secondary cities are heating up.

🧭 Murfreesboro, TN ($29.8M) and Vista, CA ($24M) are perfect examples of fast-growing Sunbelt cities drawing strategic investment.

🧳 Manahawkin, NJ ($23M) proves that even small Northeast metros can command premium pricing when development barriers are high.

Other notable deals: Vallejo (CA), Birmingham (AL), and Henderson (NV) — all showing population momentum and tight housing markets.

West Coast ≠ Cheap.

California posted three of the highest price-per-foot deals:

🏆 Costa Mesa – $387/SF

🏆 Vista – $221/SF

🏆 Vallejo – $209/SF

With limited land, dense urban cores, and high barriers to entry, it’s a pricing environment that rewards location and scarcity.

Parting thoughts

Self-storage isn’t flashy, but in 2025 it’s looking like one of the smartest places to park capital. With demographic tailwinds, supply constraints, and a clear path to pricing power, investors are zeroing in on suburban growth corridors and overlooked infill markets.

This is the playbook:

✔️ Underserved metros

✔️ Strong population growth

✔️ High barriers to new supply

Storage is more than a commodity — it’s becoming a strategic asset class.