| Kaufman Development

After another month of data, it’s clear the apartment market is settling into a summer holding pattern.

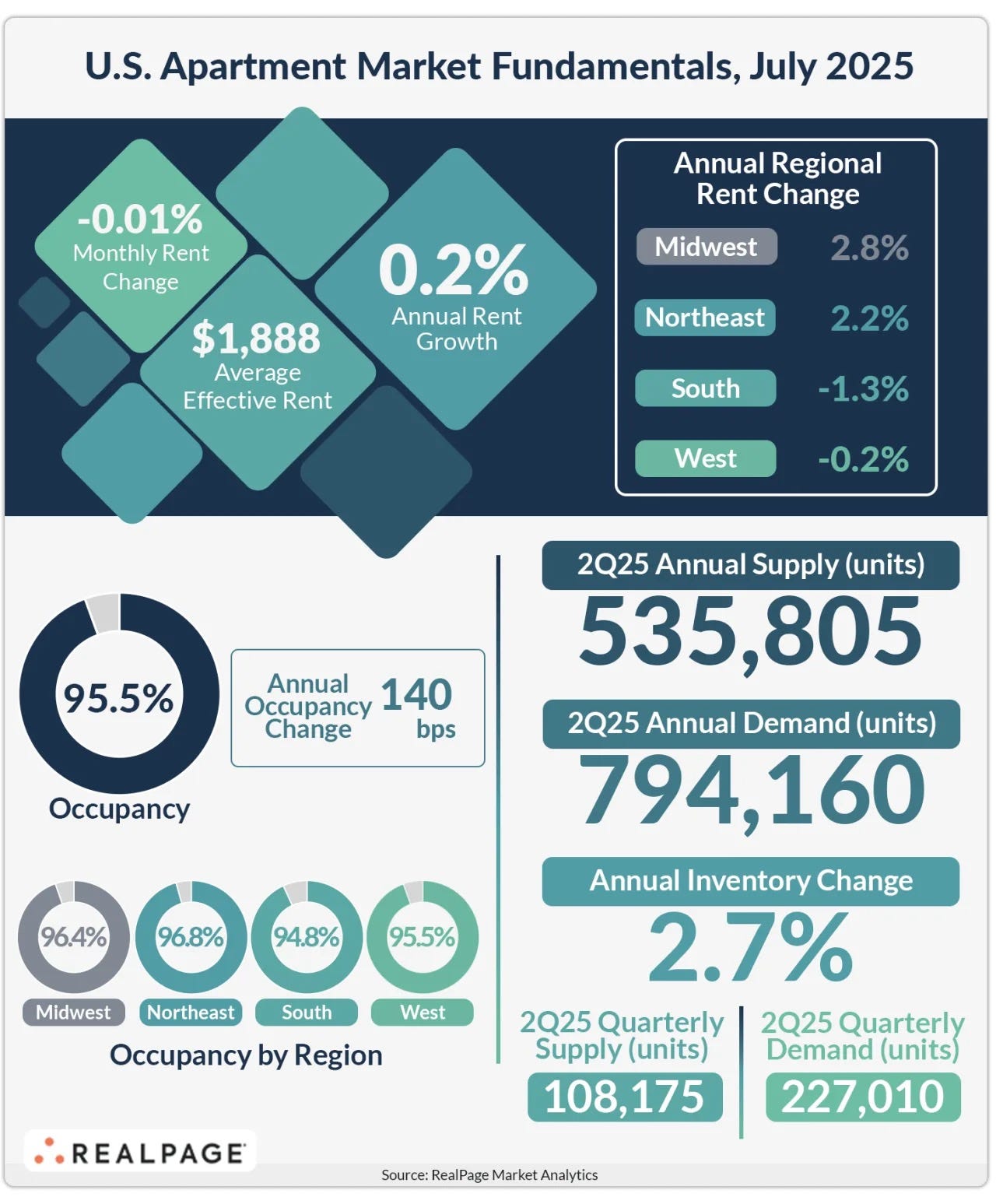

Yes, rent growth has slowed—nationally we’re seeing just 0.2% annual gains, the weakest number in nearly a year. But that’s not the whole story. What we’re seeing is not a collapse. It’s a recalibration. And from my seat as a developer and investor, that’s actually encouraging.

Let’s break it down.

Occupancy Is Holding the Line

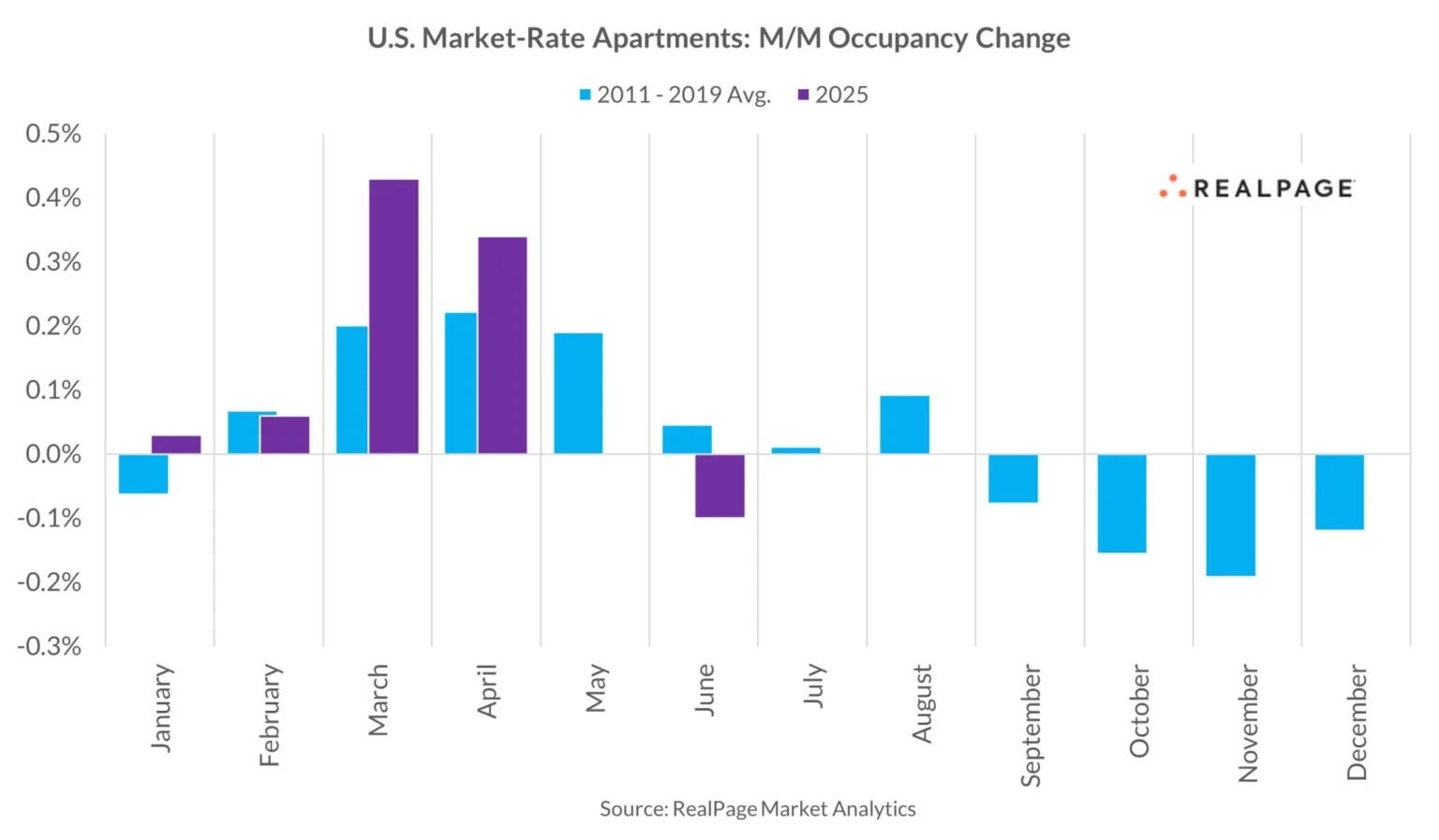

National occupancy held steady at 95.5% in July, marking two consecutive months of solid tenant retention. That’s above the five-year average and just shy of peak levels earlier this year. In other words, renters are still signing leases—just not at the breakneck pace (or price hikes) we saw in 2021 and 2022.

Smart operators are choosing to protect that occupancy rather than squeeze every last dollar in rent. It’s a classic real estate trade-off: pricing power or lease velocity. Right now, the market is voting for stability.

Absorption Is Still Red-Hot

Here’s the part that isn’t getting enough attention: we just absorbed 794,000 units over the last year. That’s a record. Even with all the talk of oversupply, demand is outpacing new deliveries. That’s not a soft market—that’s a healthy one.

And while construction completions remain elevated, they’re pulling back. Ongoing construction volume is down, and multifamily permitting is weakening, too. If you’re in the development world like I am, that matters. It means the oversupply narrative will soon fade—and rents and occupancy will have firmer footing moving forward.

Regional Dynamics Are Telling a Bigger Story

It’s a tale of four regions:

-

Northeast (96.8%) and Midwest (96.4%) are leading in occupancy, bolstered by constrained supply pipelines and dependable demand.

-

The West (95.5%) is holding the national line.

-

The South (94.8%) is starting to wobble under the weight of aggressive Sun Belt development.

On the rent side, tech-centric metros are regaining their footing. San Francisco, New York, and San Jose are posting solid annual gains, joined by surprise overperformers like Chicago, Pittsburgh, and Cincinnati.

But markets that leaned heavily on discretionary income and travel—Orlando, Nashville, Las Vegas—are the ones showing cracks. That’s not just a rent story. That’s an early warning signal about consumer behavior.

Economic Headwinds Are Starting to Show

Early 2025 brought upside surprises, but the last two months? Flat. And the data is starting to whisper what the headlines haven’t said out loud yet.

Job growth has slowed. Labor force participation is dipping. Healthcare and hospitality—two sectors that carried the recovery—are losing steam. Consumer delinquencies are ticking up. These are the kinds of signals I watch closely when underwriting deals or assessing lease-up velocity on new assets.

So far, the apartment market has weathered the storm. But the question heading into fall is whether renters are feeling the pressure—and whether that will show up in rent collections and lease renewals.

What I’m Watching

As a developer, my radar is locked on three things right now:

-

Permitting volume – It’s falling, and that’s a long-term bullish signal.

-

Tourism markets – They’re flashing yellow. I’m cautious about deals in leisure-dependent metros.

-

Rent trend lag – If macro cracks widen, rents will feel it next.

The fundamentals are still sound. But the margin for error is narrowing.

If you’re investing, developing, or even just trying to read the market right now—don’t overreact to the slowdown in rent growth. Read it as a sign of professional discipline in a maturing cycle. Focus on submarket dynamics, execution, and demand resiliency.

We’re still building. We’re just being smarter about where and when.

Daniel Kaufman