The housing market is starting to show stress fractures.

In July, nearly 36,130 properties nationwide were hit with a foreclosure filing—a 13% increase year-over-year and the sharpest annual jump we’ve seen in 2025. According to ATTOM, that means 1 in every 3,939 housing units across the U.S. is now in some stage of foreclosure, whether through a default notice, scheduled auction, or outright bank repossession.

For the first half of 2025, foreclosures are up 5.8% compared with 2024, with 187,659 homes affected. The message is clear: while homeowners still hold equity on paper thanks to high prices, growing numbers are struggling to service their mortgages.

The States Leading the Foreclosure Wave

The latest data shows a clear geographic concentration of risk:

-

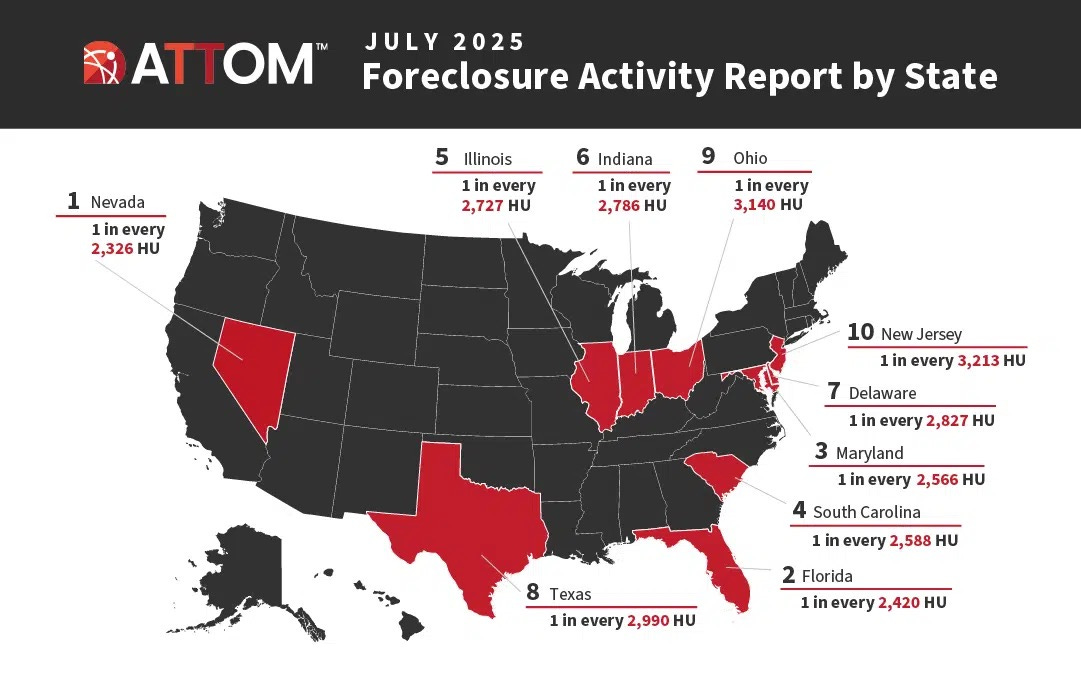

Nevada: 1 in every 2,326 homes in July faced foreclosure—the highest rate in the nation.

-

Florida: close behind at 1 in every 2,420 homes.

-

Maryland, South Carolina, and Illinois round out the top five.

In June, South Carolina briefly topped the charts, but Nevada and Florida have quickly accelerated.

Why Nevada and Florida?

Both states share an economic foundation that is more fragile than it looks: tourism.

As Realtor.com’s Joel Berner explains, economies heavily dependent on hospitality, entertainment, and leisure are the first to feel pain when growth slows. That slowdown is exactly what we’re seeing in 2025. Hotel and casino revenue softens, discretionary spending drops, and layoffs ripple through service-heavy local economies. For homeowners living paycheck to paycheck, a single income shock can mean falling behind on mortgage payments—and foreclosure filings soon follow.

It’s no coincidence that Nevada and Florida are leading the pack this summer.

Why This Matters for Developers and Investors

As a developer and investor, I view foreclosure spikes through two lenses: risk and opportunity.

-

Risk: In states like Nevada and Florida, where foreclosure filings are rising fastest, lenders will tighten credit standards. Homeowners already struggling may face difficulty refinancing, creating further downward pressure on distressed properties.

-

Opportunity: For disciplined investors, periods of heightened foreclosure activity can create entry points. Distressed assets often come with hair—legal complexity, deferred maintenance, market stigma—but in the right submarkets, they can also present strong repositioning plays.

The broader takeaway: real estate is local. National headlines don’t tell you what’s happening on the ground in Miami, Orlando, or Las Vegas. Market resilience depends not just on home prices but on employment drivers, industry mix, and the depth of local demand.

What Comes Next

Foreclosure activity is rising alongside elevated mortgage rates and slowing job growth. If economic conditions remain choppy into the fall, expect filings to increase further in tourism-heavy markets.

For investors, the key is to watch these pockets closely:

-

Which submarkets will experience prolonged distress?

-

Which assets are likely to reprice meaningfully?

-

Where will the strongest recovery occur once the cycle resets?

Those who can separate temporary volatility from structural weakness will be best positioned to act.

Final thought: Nevada and Florida’s surge in foreclosures may be the early warning system for what’s ahead. The question for investors isn’t just who’s struggling today, but which markets have the fundamentals to bounce back—and which will remain underwater.