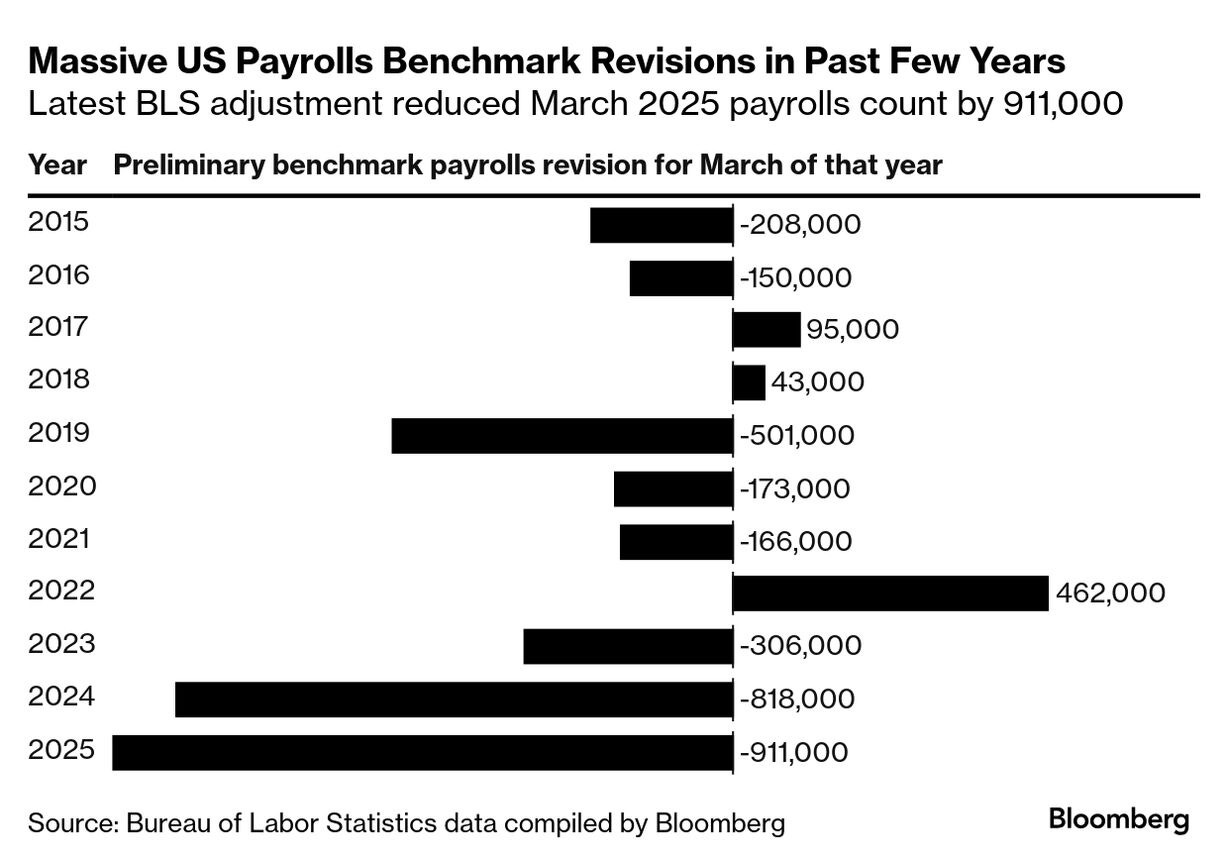

The U.S. economy is starting to feel a little shakier than the headlines might suggest. New data from the federal government shows things have been worse for American workers than we were led to believe. The Bureau of Labor Statistics’ preliminary benchmark revision—out Tuesday—indicates that payroll growth for the 12 months through March will likely be revised down by 911,000 jobs. That’s almost 76,000 fewer jobs per month on average, a stark adjustment that paints a very different picture of the labor market.

JPMorgan CEO Jamie Dimon summed it up in plain language: “The economy is weakening. Whether that is on the way to recession or just weakening, I don’t know.”

These revisions follow last week’s jump in unemployment to 4.3%, the highest level since the height of the pandemic. That’s not a catastrophic number on its own, but it adds weight to a string of recent data points showing a cooler hiring picture and rising uncertainty. The fallout has been political too—President Trump fired the BLS commissioner, citing dissatisfaction with the numbers.

Even more troubling, the BLS itself is struggling. Nearly a third of its high-level roles remain vacant, including key positions overseeing employment statistics and regional operations. That’s a tough backdrop for an agency responsible for providing the data the entire economy relies on.

Yet markets seem unfazed. Stocks closed at all-time highs yesterday, largely on hopes the Federal Reserve will step in with rate cuts. Gains in big tech—except Apple, which dipped 1.5% after unveiling the new iPhone 17 lineup—carried the S&P 500 higher even as most other shares fell. Oracle added fuel to the rally in after-hours trading with a surge in bookings. Bond markets, which had been rallying for four days, paused as traders recalibrated their expectations for rate cuts.

This split between Main Street and Wall Street is becoming more obvious. Economic fundamentals—employment, wages, and inflation dynamics—are weakening, yet financial markets are banking on easier money. That’s the tension driving investor sentiment right now.

For developers and investors, this backdrop is significant. A weaker labor market can cool demand for housing and commercial space, but it can also create opportunities to acquire assets at better pricing, lock in construction costs, and refinance projects if rates fall. Risk is rising, but so is the potential upside for those positioned to take advantage of volatility. The challenge will be separating structural shifts from short-term noise, and that’s where disciplined underwriting and long-term vision will matter most.