When you’ve been in real estate as long as I have — through multiple cycles, multiple recessions, and more than a few false bottoms — you learn to appreciate the quiet moments. The ones that don’t make headlines but mark the turning points. That’s what Q2 2025 feels like.

No fireworks. No collapse. Just… balance.

According to MSCI’s latest data, commercial real estate pricing stayed flat from May to June. The RCA CPPI US National All-Property Index dropped just 0.7 percent year-over-year. And in this environment, that kind of stillness is newsworthy.

This isn’t just statistical noise. It’s a signal: the market is recalibrating. We’re not fully out of the woods, but we’re no longer tumbling downhill either.

Deals Are Moving Again

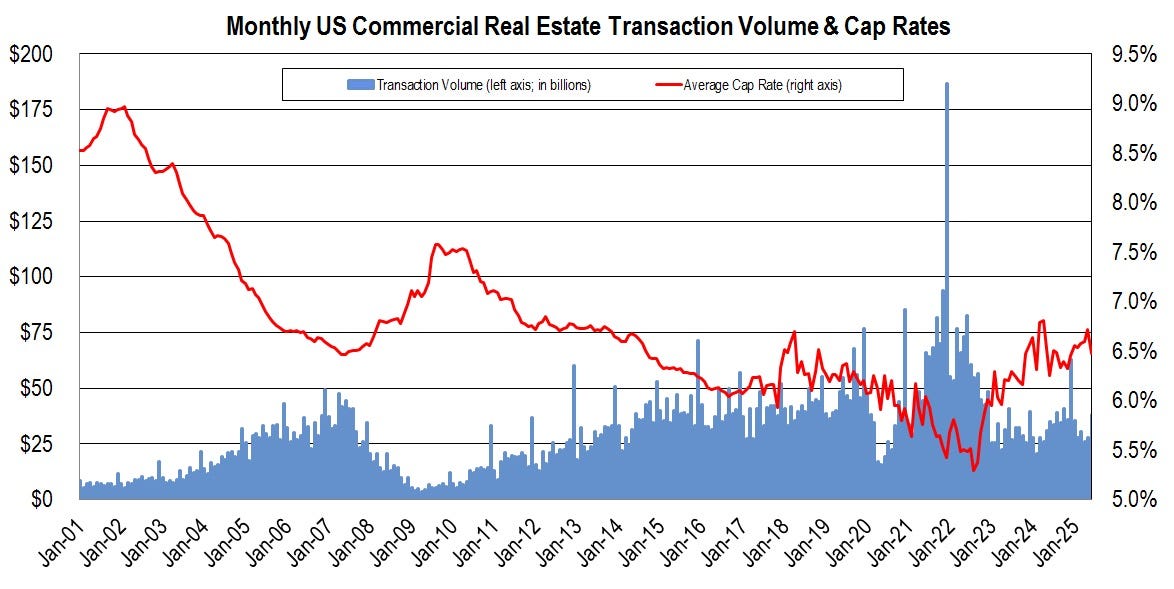

One of the clearest signs of momentum? Transaction volume. MSCI’s revised Q2 figures show a 29.6 percent year-over-year increase — a sharp turnaround driven by renewed activity in retail, industrial, and yes, even office.

Cap rates inched down to 6.48 percent in June, with meaningful compression in office (down 32 basis points) and multifamily (down 18 basis points). That’s not just rate movement — that’s investor confidence trickling back in.

Multifamily: Stabilizing, Not Soaring

Multifamily finally posted a year-over-year price gain — a modest 0.1 percent, but still the first positive print since 2022. Prices are down 0.2 percent since March and remain a full 18.5 percent below their peak, but there’s clearly a floor forming.

Lower financing costs from last year’s rate cuts are starting to show up in pricing, and buyer sentiment is beginning to thaw. I’m not calling a rally, but the ice is breaking.

Office Is Still in Rehab

Office remains the slowest horse in the race, with prices down 1.9 percent year-over-year. CBD office continues to feel the pain, falling 4.2 percent, versus a 2.1 percent dip in suburban — but here’s what caught my eye:

This is the narrowest spread between CBD and suburban office performance since mid-2022. That could mean we’re approaching price discovery — or at least a shared sense of where bottom is.

Retail and Industrial Keep Carrying the Load

Retail led all sectors with 3.5 percent annual price growth — holding steady month-over-month. Industrial followed with 1.6 percent annual growth, continuing its quiet strength with gains from both May and March.

These sectors are still riding the structural tailwinds we’ve been talking about for years: omnichannel retail, logistics, last-mile distribution, and neighborhood-scale service centers. These aren’t “hot” plays — they’re resilient, cash-flowing real estate. And in today’s climate, that’s gold.

What I’m Watching Next

The Fed is showing more predictability, rates are leveling off, and lenders are back at the table — albeit cautiously. That gives developers and investors room to underwrite with more clarity, even if the return-to-growth narrative is still uneven.

In my world, we’re seeing this play out on the ground: land deals getting inked, multifamily projects repriced but proceeding, and value-add retail attracting fresh capital. The tide isn’t racing back in, but it’s no longer receding.

The Bottom Line

Flat is the new up.

And in a market that’s been anything but stable over the last two years, that’s progress.

We’re not celebrating just yet — but we’re building again. And that’s exactly where you want to be when the next leg of the cycle begins.

Daniel Kaufman is a real estate developer and investor with over $2 billion in projects delivered nationwide. He leads Kaufman Development, Elevation Redevelopment, and the Kaufman Family Office. More at www.dkaufmandevelopment.com and www.elevationredev.com.