The headlines this week might seem distant from the ground-level work of building and investing in real estate—but ignore them at your peril. A high-stakes legal showdown over Donald Trump’s tariff authority, a surprise inflation report, and signs of a stalling labor market are all converging in ways that directly impact development strategy, construction pricing, and capital markets behavior.

Let’s break it down.

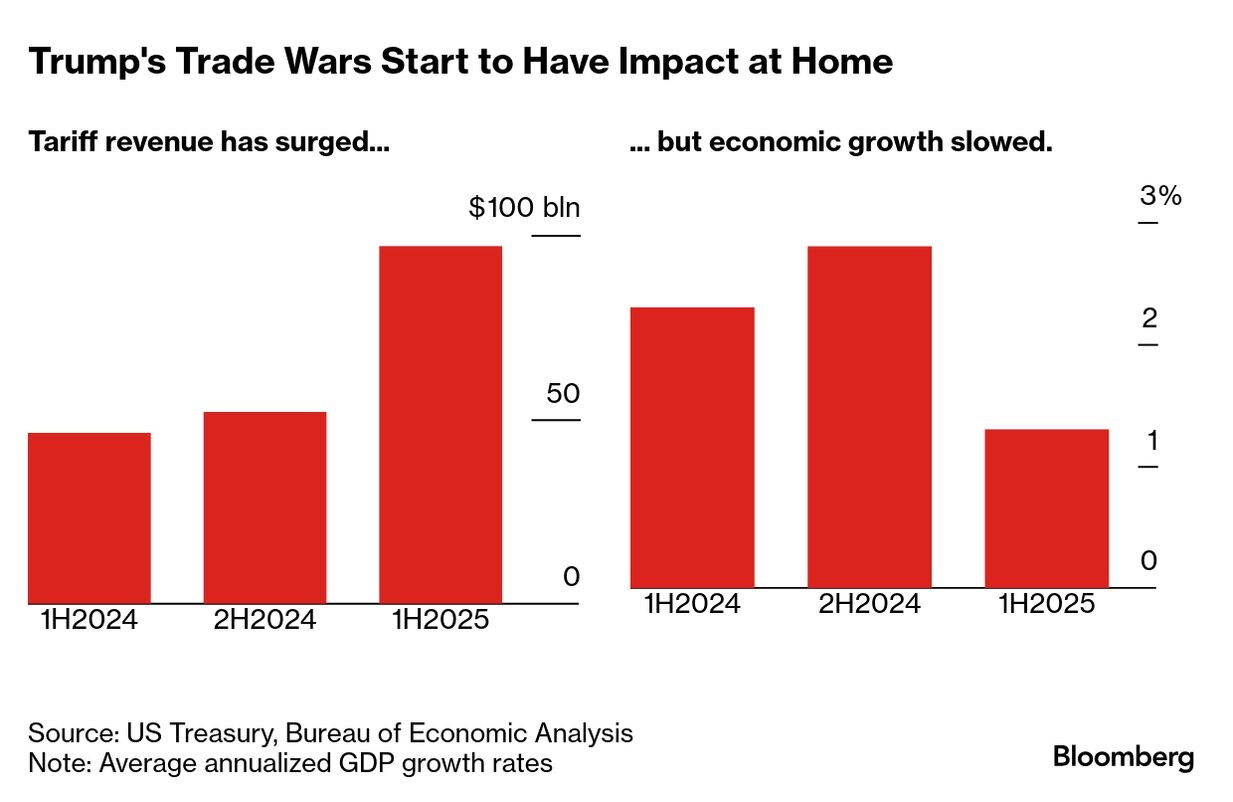

The Tariff Tug-of-War: Why It Still Matters

This week, a federal appeals court heard arguments challenging Trump’s use of the International Emergency Economic Powers Act (IEEPA) to unilaterally impose tariffs. The lower court already ruled the move unconstitutional—and now the full circuit is weighing whether the president overstepped his authority.

For developers and investors, this isn’t some abstract legal skirmish. Tariffs have real, measurable effects on construction materials, supply chains, and investor sentiment. Just ask anyone trying to budget a project with steel, glass, or imported fixtures. If the courts ultimately side with the plaintiffs, it could curtail future unilateral tariff moves, introducing some much-needed stability into a market where policy risk has become another line item in the pro forma.

But even if Trump loses this round, the game isn’t over. The case will likely be stayed, giving the Supreme Court—currently a 6-3 conservative supermajority—time to weigh in. And historically, they’ve been more than willing to greenlight the former president’s agenda.

Bottom line: Even the legal mechanisms governing tariffs are in flux, and the risk of economic disruption from future trade wars remains very real.

Inflation Is Stubborn—and So Is the Fed

While legal minds debated presidential power, the Federal Reserve’s preferred inflation gauge—the core PCE index—ticked up again in June, rising 0.3% month-over-month and 2.8% annually. That’s one of the fastest monthly paces this year.

For those of us actively underwriting deals, the cost of capital remains front and center. Persistent inflation gives the Fed cover to hold rates higher for longer—even as deal volume slows and cap rates adjust. It’s a tension we’ve been living with for over a year: fundamentals are softening, but financing costs haven’t followed.

Consumer spending, meanwhile, is barely growing. Disposable income is flat. Wage growth is cooling. And the saving rate is stuck at 4.5%, leaving little room for surprise retail strength. This isn’t a robust economic engine—it’s a sputtering one.

What Developers and Investors Should Watch

Here’s what I’m paying attention to right now, and what I’d suggest you build into your models:

-

Material pricing volatility is still being driven by geopolitics, not just demand cycles.

-

Entitlement timelines and delivery schedules need to include margin for legal or policy disruption.

-

Rate sensitivity among buyers and renters is accelerating, especially in projects with premium positioning.

-

Private capital is still available, but it’s slower, more cautious, and laser-focused on downside protection.

A Final Note on “Predictable Chaos”

In classic Trumpian fashion, the same week he said there’d be no extension of his August 1 tariff deadline, he… extended it. Again. This time the favor went to Mexico.

Whether you’re a Republican, Democrat, or proudly unaffiliated, what matters for our business is that policy unpredictability continues to shape investor psychology and asset pricing. If you’re not factoring that into your investment thesis—or the way you communicate with LPs—you’re missing the mark.

As always, we’re operating in a market that rewards discipline, creativity, and adaptability. Keep your ear to the ground, your risk models updated, and your LPs close.

See you out there,

Daniel

📬 Subscribe to stay updated on market moves, policy shifts, and how they affect real estate developers, investors, and builders on the front lines.

Let’s build smarter.