The labor market is officially sending a distress signal. August’s Nonfarm Payrolls data came in well below expectations, unemployment is creeping higher, and for the first time in this cycle, there’s a one-to-one ratio of unemployed workers to job openings. The picture is clear: the Fed now has cover to pivot.

The Jobs Data: A Slowdown That Can’t Be Ignored

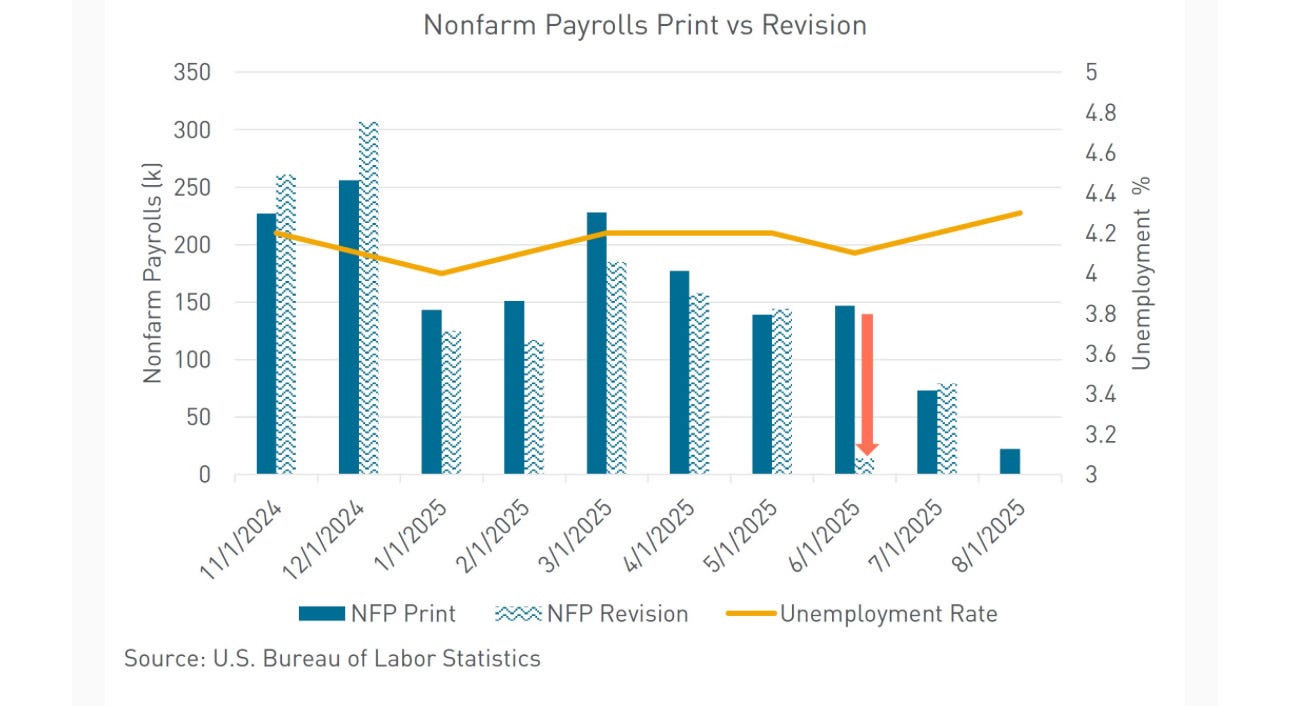

Payrolls rose by just 22,000 in August, well short of the 75,000 economists had penciled in. The unemployment rate climbed to 4.3%, matching the highest level in this cycle. June’s data was revised sharply lower, turning a modest gain of 14,000 jobs into a net loss of 13,000—evidence that the slowdown is deeper than initially thought.

Over the last three months, job growth has averaged just 29,000 per month, the weakest stretch since the pandemic. Even sectors that have been stalwarts—like health care and leisure and hospitality—show signs of cooling. Health care added 47,000 jobs, but that’s the smallest monthly gain since early 2022.

Meanwhile, federal government payrolls fell by 15,000 in August and are down 97,000 jobs year-to-date, reflecting the administration’s push for efficiency and spending restraint.

JOLTS Shows a Cautionary Shift

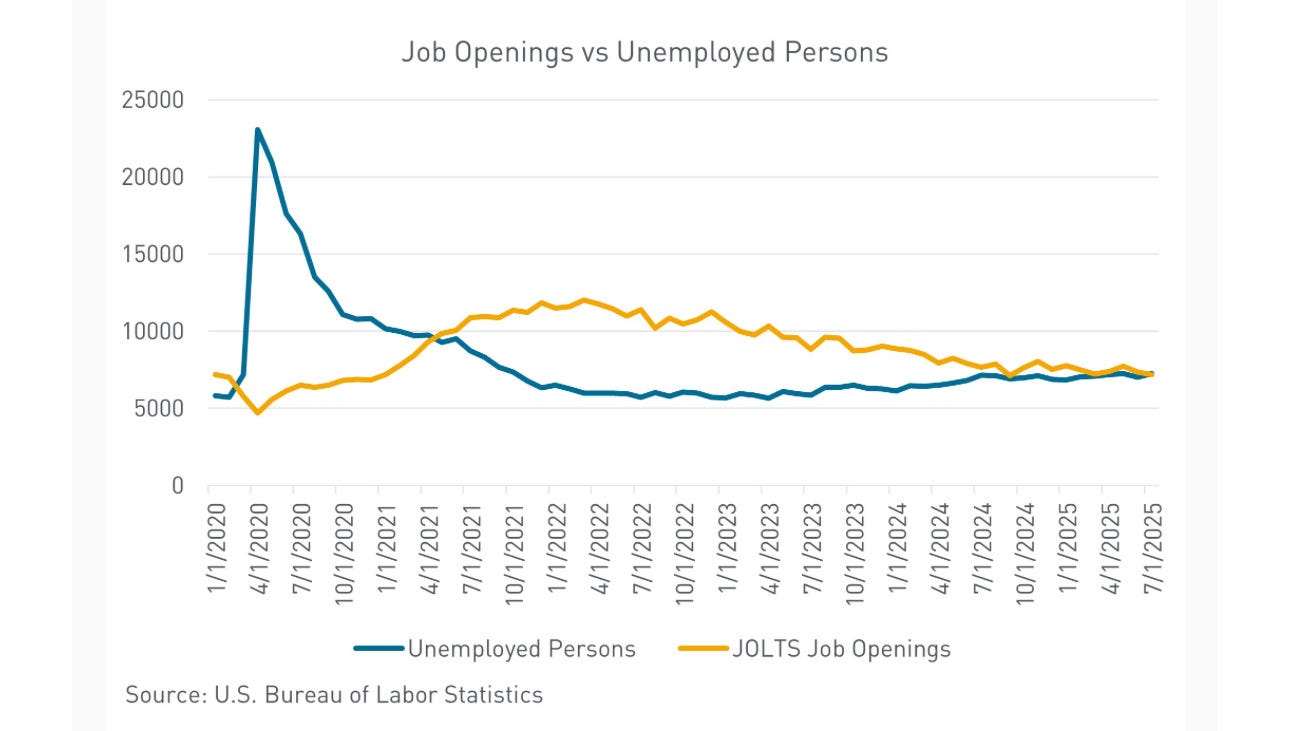

The July JOLTS data confirmed what many business leaders have been feeling: hiring is slowing, and employers are becoming more selective. Job openings fell to 7.18 million, a 10-month low, with notable declines in health care, retail, and hospitality.

Perhaps most importantly, the ratio of job openings to unemployed workers is now 1:1. In 2022, that ratio peaked at 2:1, illustrating a much tighter labor market. Fed officials closely watch this metric as a gauge of labor demand, and its steady decline signals that the labor market is no longer a driver of inflationary pressures.

What This Means for the Fed

The Federal Reserve has had two months of data since its last meeting, and the message is consistent: growth is cooling, hiring momentum has slowed dramatically, and businesses are bracing for uncertainty. Inflation remains murky, but the labor market gives policymakers political and economic justification to resume cutting rates.

Markets are now pricing in a September rate cut as a near certainty, and traders have increased bets on two more cuts this year. Treasury yields have already responded, with the 10-year yield dropping nearly 20 basis points since Labor Day.

This is a major shift in monetary policy, one that could bring relief to credit markets and real estate financing, but it’s also a signal that the Fed is worried. The days of a “soft landing” narrative may be behind us.